I know that as firefighters and paramedics we do not think of ourselves before we think of the citizens we serve. We do work hard for the salary and benefits we have earned. We must bring that same attitude that we respond to emergency calls with to the question of our pensions. In the end, if our pension system fails, it is those very same citizens, and our children and grand children that will be stuck with the oppressive taxes needed to pay our pensions. The cutting of services so severe it would effectively eliminate almost all other state services is also another option. The third option is to increase our contribution rate and future firefighters contribution rates to such excessive amounts, as to be unrealistic. We owe it to our citizens and we owe it to ourselves to look at the facts, and make-needed changes.

We are supposed to be able to work hard in our life and achieve a level of success suitable to each of us as individuals. To achieve contentment in life where ever or what ever that is for each of us. We are supposed to be able to do that without interference from the government. The most effectively run government is the one you almost never have to think about or be involved with except to elect your leaders at certain intervals. At those times we are expected to make informed decisions on who we want to lead us and then go back to living our lives, chasing our pursuit of happiness. There are times in history though that requires us to pay closer attention, to be more involved. There are times when we must look above our daily lives and look at the bigger picture because it has been twisted and screwed up so bad that it is going to have a direct effect on our lives. We must make informed decisions.

Most of us have been a sleep at the wheel, because our lives have been good. This is okay, this how our system is supposed to work. However, a lot of us are just now being awoken to the calamity that is our current state of affairs. We are just now awakening because it has just now started to effect us individually in our daily lives.

It is more important now to become informed, because there are powerful forces in our society, and globally that are trying to change the very core principals that have made our country what it is. As a member of a labor union you are involved in this battle for the future of America whether you realize it or not. If you do not believe this is true, if you do not believe there might be an ounce of truth to this, then change the page; go back to what you were doing because we don’t really have the time to convince you. If you are one of the many who do understand this read on, because our National Labor Leaders have put us on the wrong side of this battle. I don’t know about your local leaders, but mine have swallowed what the national and international organizations are putting out, hook line and sinker. We tried to address these issues through our locals, and with our local leaders only to be silenced with parliamentary maneuvers and out and out manipulations. There will be no dissenting from the party line! So we are forced to go about it in a public way, so be it.

We are told to stand up, take this sign, protest against these people because they want to take your pension. I hear one side saying we need to reform these pensions systems (reform not take) because they are unsustainable. Then I hear the other side, the side I pay my money to, saying your pensions are stable they are funded, its just an excuse to come after the middle class, and take your pensions to enrich themselves. Since I cant get anything but hyperbole from either side I must do the research myself and come to an informed decision. The following is what I found.

This information is based on a brief compiled by NASRA (National Association of State Retirement Administrators) titled “Public Pension Plan Investment Return Assumptions”. This information comes from an organization of people who most definitely have a vested interest in the pension systems being “stable”.

There is a debate in our country right now on how to measure the future returns on our pension systems investments. I do not know about you, but when it comes to something this important, I would like to have the facts, so I can make a judgment on who to believe.

This is an extremely important debate to us, because the end result will reveal just how stable or unstable our pension system is. This measurement is vitally important because, of the monies needed to make the pensions current liabilities 60% come from the money the pension system makes on its investment. To put it another way, right now our pension system could only make 40% of its obligated payments this year if it only used the money contributed by us, and our employer combined.

One side of the debate says that what we currently use, the “historical returns on assets” is the correct method. When this method is used the pensions system appears to be in pretty good shape, and the unfunded portion of the liabilities are in the 700 billion dollar range. This is bleak, but not catastrophic. The other side says we should use what is called a “riskless” rate of return based on more secure assets like bonds, and treasuries. When this method is used the unfunded liabilities sky rocket to the 3 trillion dollar area. This is catastrophic.

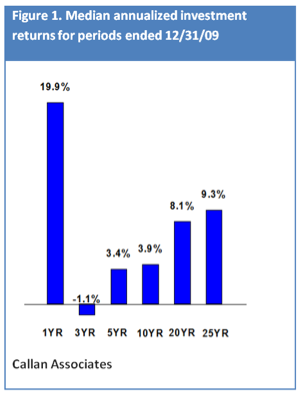

Let’s look at the “historical returns on assets” side of it. Currently a large majority of pensions systems use an expected 8% return on investment to predict their future stability.

According to NASRA this gives the pensions system a 50/50 shot of making its obligations or coming up short. Since this predictor is based on historical trends, then we should then look at what the historical trends are.

As you can see, over the last 25 years there has been a better than 8% return. This is what the people on this side of the debate point out to justify their position. Keep in mind that this still represents an estimated shortfall of $700 Billion.

The other side says, we shouldn’t use the historical returns on assets because our pensions are guaranteed, and must be paid with either tax increases or spending cuts or a combination of both. This side says that using the historical returns data is covering up a huge unfunded liability that runs in the 3 trillion dollar range. They want to tie it to more stable return assets like bonds and treasuries that would give a return of 4%.

The following are all quotes taken directly from the NASRA brief.

Because no one knows what the future holds with respect to economic and other contingencies, the best an actuary can do is to use professional judgment to estimate possible future economic outcomes based on past experience and future expectations, and to select assumptions based upon that application of professional judgment. rather than one specific assumption. The actuary should determine the best‐estimate range for each economic assumption, and select a specific point from within that range. In some instances, the actuary may present alternative results by selecting different points within the best‐estimate range.

Although investment return assumptions used by public pensions are

intended to reflect long‐term considerations, they are not static, and

they do change. Until the 1980s, a majority of public pension assets were

invested in bonds and other asset classes that yielded a lower projected

return than a diversified portfolio of stocks, bonds, real estate, etc.

Investment return assumptions were commensurately lower. First in

response to high interest rates during the late 1970s and early 1980s,(emphasis added)

(*authors note* what do you think will happen to the interest rates when the FED and the Treasury Dept. begin to try and suck back out all the extra money it has printed in the last 2 years?)

As the standard disclaimer says, past performance is not an

indicator of future results.

Lets analyze this data. In the last 25 years we have had a return on investments at about 9.3%, but this average includes an extremely good time that is about to drop off the 25-year mark. When this happens, when you look at the next “last 25 years rate on returns” it will be catastrophically worse. We have only been in this more risky area for the last 25 years, prior to that we were in the safer bond market, so we really only have one point of data to measure how stable it really is. The 8% estimate gives us a 50/50 shot of making it or not. Since NOBODY can predict the future let’s just try to give it a good guess.

If you look back at the return on investment graph you will see that although over the last 25 years there has been 9.3% return, over the last 10 years there has only been 3.9% return. So what it comes down to is what you think the next 10 to 15 years is going to do. Are we going to continue with the less than 4% (which remember is catastrophic) returns, or will it get better.

The following quotes were taken from various research papers from the Center for Retirement Research at Boston College, or CRR. In the interest of brevity the authors of these papers can be found by looking up these articles with the date and title on the CRR website.

The Impact of Public Pensions on State and Local Budgets, #13 October 2010.

- “Pension contributions are likely to account for a larger share of state and local budgets in the future than in the past for a number of reasons. First, states and localities have relied on a rising stock market to increase funding, and a repeat of the 1982-2000 stock market boom is unlikely.” (Emphasis added).

Valuing Liabilities in State and Local Plans, #11 June 2010.

- - “Most economist contend that the discount rate should reflect the risk associated with the liabilities, and given that benefits are guaranteed under most state laws, the appropriate discount factor is a riskless rate, roughly 5 percent.”

- - “given their guaranteed status, state and local pension liabilities should be discounted at a riskless rate and shows how much measured liabilities would increase by applying such a rate.”

- - “the argument is compelling (emphasis added) that the liabilities of public pension plans, which are guaranteed under state law, should be discounted by a rate that reflects their riskless nature”.

The Funding of State and local Pensions: 2009-2013, #10 April 2010.

- - “after 2009, the funding picture will continue to deteriorate to the extent that years of low equity values replace years of higher values”

- - “2010 actuarial reports will show assets equal to about 77 percent of promised benefits What happens thereafter depends increasingly on the future performance of the stock market. Under the most likely scenario, the funding ratio will continue to decline as the strong stock market of 2005-2008 is slowly phased out of the calculation. By 2013, the ratio of assets to liabilities is projected to equal 72 percent” This paper also gives a optimistic out look that says by 2013 they will be funded at 76%, and a pessimistic out look that says they will be funded at 66%.

- - “The ultimate outcome will depend on the performance of the stock market, but under our most likely scenario, funding ratios will decline to 72 percent by 2013”

This information comes from a source that does not have a vested interest in whether or not a pension system is considered stable.

On a much more interesting note, for comparisons here is some information on my retirement system. According to the 2010 Popular Annual Financial Report has a ranking in the top 28% for return and bottom 28% for risk. This meaning it is one of the better off systems.

According to NVPERS Popular Annual Financial Report Fiscal Year Ended June 30, 2010 as of June 30, 2009 it had a funding level of 72.5%, and as of June 20, 2010 70.5%. Keep in mind that these numbers are based on a “rosy picture” estimate of 8% on return. (If you didn’t catch it, that means we are ALREADY below what we are projected to be at by 2013)

This report also shows that there is a continuing trend of having less and less employees to support even more and more retirees with even larger and larger pensions. Given the fact that I see with my own eyes brothers and sisters in my own union working the computerized staffing system to “spike” their compensable retirement wage, and I only see one of my local union leaders speaking out about it, and given the fact that when rank and file members try to speak out about it, they are silenced by department administration and the rest of the locals leadership, taken all of this into account, I personally do not see a “stable” future for our pension system.

This is why politics are so important, they affect everything. What is it you believe? I posed this question to a colleague the other day, and he acted like it was an absurd question. It really is this simple, and it comes down to the very question that is being proposed to the nation in the next election cycle. Do you believe that we will be better off, and the economy will restore itself under big government, tax the rich, wealth redistribution policies. If you believe this then go pick up your sign and “protect” your pension.

However if you believe as I do, that smaller government, tax cuts, and more freedom with less government intrusion is what will stimulate the economy then you must speak out about it. Our union leadership has made it clear where they stand. What I hope this article does is make you painfully aware that even if you’re uninterested in the political discussion, your future depends on it.

When I take these following things into account;

- - that Richard Trumpka the President of the AFL CIO recently said that he did not get into the labor movement to negotiate wages and benefits but that he got into the labor movement as a vehicle to advance a progressive agenda

- - The progressive agenda is to expand government, destroy free enterprise, and redistribute wealth.

- - People with vested interest are telling me my pension is ok.

- - People with out vested interest are showing me that my pension system is not looking so good.

- - Self identified “progressives” continually trumpet “never let a good crisis go to waste”

When I evaluate all those things it makes me question the following?

- - Are my national labor organizations looking out for my interest or are they trying to “protect” the next looming “crisis” they can use to further the progressive agenda.

- - Has my local union leadership and I been duped? Are we being used?

It looks to me that we have and we are.

You certainly have done the homework. I do imagine that the progressives when and if they get to take over and make this country a socialistic State will give everyone a fair and equable pension. Or should I say that is what they plan on doing with their god intenions. However you are right they shoot themselves in the foot by distroying what fuels the revenue. Free enterprise, and captatlism. Great work!! I hope to read more from you. I have posted this website on my face book page. I saw a comment of yours on the Blaze.

ReplyDeletewww.josephfawcettart.com western artist